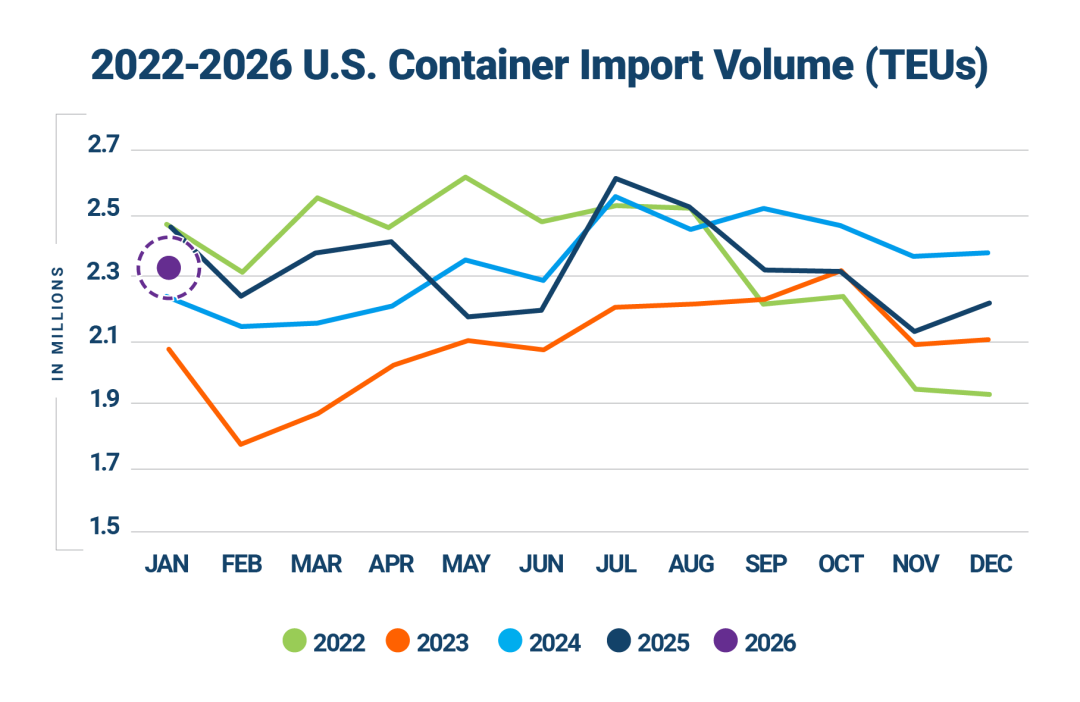

According to Descartes data, in January 2026, the total container import volume in the United States increased by 4.1% month-on-month to reach 2.319 million TEUs, showing a 6.8% year-on-year decrease. Despite the year-on-year decrease, this figure is slightly higher than the six-year average and represents an 11.8% increase compared to January 2019.

In January 2026, container imports from China to the United States increased by 9.3% month-on-month but decreased by 22.7% year-on-year, totaling 771,000 TEUs. This is a 24.6% drop compared to the historical peak of 1.023 million TEUs set in July 2024. China's share in U.S. container imports rose from 31.7% the previous month to 33.3%.

Regarding ports, in January 2026, the container import volume at the top 10 U.S. ports increased by 4.9% month-on-month, adding 92,150 TEUs.

Market share in the U.S. East Coast and Gulf Coast ports increased, while the market share of U.S. West Coast ports slightly decreased. In January 2026, the market share of the top 5 West Coast ports decreased from approximately 44.0% to 43.4% (-0.6%). The market share of the top 5 East Coast and Gulf Coast ports slightly increased to 40.8%.

Overall, the top 10 U.S. ports accounted for 84.2% of the total container import volume in January, slightly higher than December's 83.3%.

In January, there was some improvement in the delay situation at major U.S. ports. Overall, the major U.S. ports continued to efficiently handle cargo throughput without significant signs of congestion.

Descartes analysts pointed out that the escalation of tensions between the U.S. and Iran has increased maritime risks in major sea lanes. The reopening of the Red Sea may reshape the global shipping landscape in 2026. Industry attention is shifting towards the potential reopening of the Red Sea and Suez Canal corridor in 2026. The unbalanced reopening and persistent risks may delay a comprehensive network reset, keeping maritime trade planning and freight prospects volatile in 2026.

China——Brazil Trajectory Tracking

+86 532-85066033/34